Basics of Patient Compensation Funds By State

Gallagher Healthcare :: Industry Insights

By Dean Gereau | 4/29/2015Medical liability claims generate monetary and non-monetary costs to society, making it essential to examine their significance. Patients suing providers for malpractice is not uncommon, with 34% of physicians experiencing a lawsuit for an act of malpractice and 16.8% being the subject of multiple malpractice cases in 2017.

Ultimately, medical malpractice is costly to everyone. About 210,000 to 400,000 people die each year due to medical errors in hospitals across the United States. Some patients suffer serious complications or injury due to error or malpractice. For doctors, medical malpractice insurance can cost $250,000 per year, on average.

Given these high percentages of lawsuits regarding medical malpractice, states, hospitals, attorneys and medical professional associations have many solutions for reducing medical malpractice incidents, lawsuits and high premium costs for doctors. One of the ideas that has emerged since the 1970s to address these issues is that of the patient compensation fund, or PCF.

If your professional practice is in one of the eight states with PCFs, you need to understand what PCFs are and how they can affect your malpractice insurance and the process in the event of an alleged instance of medical error.

We have compiled this handy guide to help you understand what a patient compensation fund is and how it can affect your physician insurance. If you have any specific questions, don’t hesitate to contact Gallagher Healthcare to discuss your own insurance needs as a healthcare practitioner.

What Is a Patient Compensation Fund (PCF)?

A patient compensation fund offers a cost-effective and reliable medical malpractice coverage option for all participating private healthcare providers in a state. With this fund in place, it becomes an excess insurer. Providers are financially responsible for up to a certain amount per claim. They can use the patient compensation fund for additional coverage and set a limit on damages.

Many providers partake in the patient's compensation fund and must pay an annual surcharge for the protection and coverage they receive. Healthcare providers who participate in patient compensation funds must also maintain liability limits at the threshold amount specified by their coverage.

PCFs function in much the same way as standard, commercial professional liability insurance in that large populations of insureds all contribute a “surcharge” (the PCF version of policy premiums) to the fund, which then pays out to patients with valid claims. However, several key differences exist, as these funds are operated by their respective states and work in conjunction with a physician’s primary professional liability insurance policy, rather than replacing that policy.

History of Patient Compensation Funds

In most states, PCFs were first established in the 1970s. The funds were created in response to what was called a “medical malpractice crisis,” so termed because an increasing number of healthcare practitioners cited difficulty in securing medical malpractice coverage or reported prohibitively high premiums.

PCFs were designed to address this problem by reducing doctor liability in medical malpractice cases without reducing the protections injured patients could receive. In reducing physician liability, PCFs were created to lower costs for medical practitioners. By 1979, fifteen states had adopted the medical malpractice patient compensation funds.

How Do Patient Compensation Funds Work?

A healthcare provider is required by law to carry malpractice insurance to protect the professional or facility from lawsuits and to provide patients with protection from expenses caused by medical errors. In most states, a patient compensation fund works with this insurance. A surcharge on medical malpractice insurance premiums goes into the fund.

In the event of an alleged medical error, a patient’s case is examined. If the case is found to qualify and to be legitimate, medical malpractice will cover the injured patient’s costs to a specific limit. The rest is paid by the PCF if the doctor was participating in the PCF. In some states, such participation is mandatory. In others, it is up to the physician or medical professional to decide to join.

What Is Medical Malpractice Liability?

Medical malpractice is any injury claim involving negligence from a doctor, surgeon, nurse or other healthcare professional. Proving a patient is a victim of medical malpractice requires evidence from the plaintiff to demonstrate that they suffered medical injuries due to a medical provider's breach of professional duty. Examples of medical malpractice include giving inaccurate prescriptions and performing incorrect surgery.

Medical malpractice liability refers to a person or parties legally responsible for patient injuries. However, it can be hard to determine which party is more liable in some cases. For example, a doctor and their nurse can both contribute to medical malpractice, resulting in the lawsuit splitting between both parties. If the doctor or nurse gave the wrong instructions and the other party failed to correct the inaccurate instructions, a medical malpractice case may consider both parties responsible.

A hospital can also face liability for malpractice, especially when the overall policy or quality of care is below a specific standard.

Which States Have Patient Compensation Funds?

Patient compensation fund states vary widely by rules and regulations. The following list of patient compensation fund states explains the caps and regulations for each state’s fund program:

Jump to: Pennsylvania | Wisconsin | Kansas | Indiana | Louisiana | New Mexico | Nebraska | South Carolina | New York

1) Pennsylvania Patient Compensation Fund

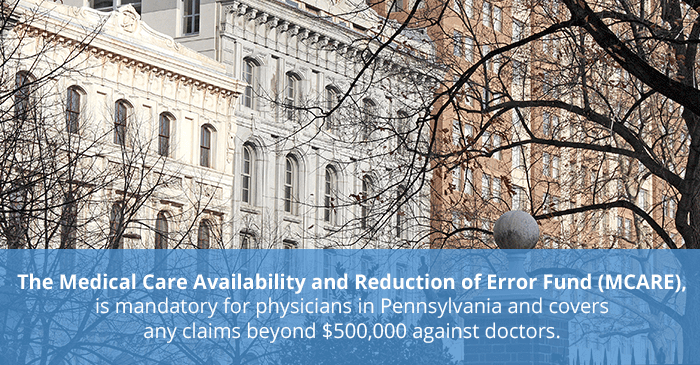

In Pennsylvania, the Medical Professional Liability Catastrophe Loss Fund was established in 1975 as a type of PCF, but in 2002 its successor was introduced: The Medical Care Availability and Reduction of Error Fund (MCARE). MCARE is mandatory for physicians in the state and covers any claims beyond $500,000 against doctors. However, MCARE is evaluated regularly and will eventually be phased out as the limit of coverage for private insurers will increase. The phasing out of the PCF is partly due to the fund’s $2 billion in deficits.

2) Wisconsin Patient Compensation Fund

Established in 1975, the Wisconsin Patients’ Compensation Fund covers all patient costs and awards above the insurance limits of a provider’s insurance. All healthcare providers in the state must have a medical malpractice coverage of $3 million, including a limit of $1 million per claim. Claims above this amount are paid by the fund. To take part, physicians must pay an annual amount to take part in the PCF. To secure money from the fund, plaintiffs who think their suits may exceed caps on insurance must become part of the lawsuit which also includes the PCF as a party.

In 2014, Wisconsin plaintiff payouts in medical malpractice cases were among the lowest nation-wide, and the state also had the largest PCF across all states, with over a billion dollars.

3) Kansas Patient Compensation Fund

In Kansas, medical facilities such as hospitals are required to take part in the PCF, known as the Health Care Stabilization Fund. Private insurance companies are the ones who gather the surcharges from hospitals and other participants and submit the money to the state treasury, where the money is kept apart from the rest of the budget.

In the event of a malpractice claim, the fund pays any amounts exceeding the insurance coverage of a medical provider. In cases where the claim amount is over $300,000, the money may be paid out to injured patients in yearly installments, which include interest.

4) Indiana Patient Compensation Fund

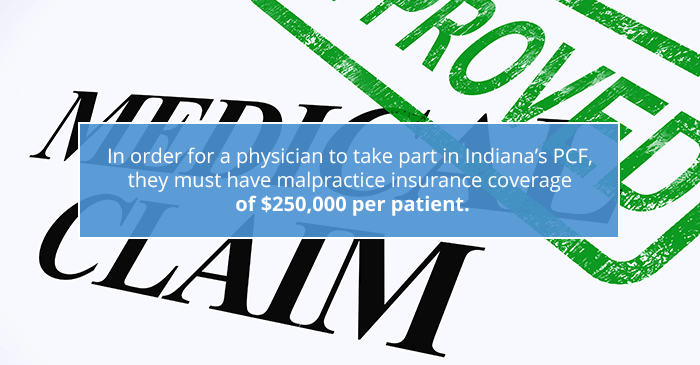

In Indiana, the PCF was established in 1975, and in 2015, the state’s cap on medical malpractice insurance claims was $1.25 million. Private insurers in medical malpractice claims pay the first $250,000, and the PCF pays any amount over that, although not more than $1 million. State laws also prohibit attorneys in malpractice cases from claiming more than 15% in fees from any amount awarded by the PCF.

In Indiana, state law does not absolutely require physicians to maintain malpractice coverage. However, most hospitals and other places of employment do require it. In order for a physician to take part in the state’s PCF, they must have malpractice insurance coverage of $250,000 per patient.

If a patient is injured in Indiana and wishes to file a medical malpractice claim, he or she must first submit to an evaluation of their case by filing a proposed complaint before the Indiana Department of Insurance. Three physicians make up a medical review panel to look at the claim and to determine whether the claim has merit. Once the panel has conferred, the panel issues a report, and the patient can determine whether to proceed with their legal claim.

5) Louisiana Patient Compensation Fund

The Patient’s Compensation Fund was established in Louisiana in 1975, and most health care practitioners in the state take part by paying surcharges through their insurance. Participation is not mandatory, however. Money for the fund is kept separate from the rest of the state’s budget. In Louisiana, private insurers cover the first $100,000 of a claim through a security deposit or private insurance, and the state fund covers the rest.

6) New Mexico Patient Compensation Fund

In 1976, the New Mexico Medical Malpractice Act created the state’s PCF. Currently, the fund is administered by the Superintendent of Insurance and a variety of medical professionals can apply for participation, including:

- Doctors

- Nurse anesthetists

- Physician’s assistants

- Hospitals

- Chiropractors

- Podiatrists

- Outpatient healthcare facilities

Under the fund, punitive damages and medical care are not capped, but awards are capped at $600,000. Before any awards are made, medical malpractice claims are reviewed by the New Mexico Medical Review Commission. Under the laws of the state, healthcare providers who are members of the PCF cannot be sued after a three-year period has passed (unless the plaintiff is a child under the age of six).

7) Nebraska Patient Compensation Fund

In Nebraska, the Excess Liability Fund is available to those health care professionals who qualify under the Hospital-Medical Liability Act. Private insurance covers the first $500,000 of a claim, and the fund pays the rest. However, there is a total cap (including fund payment and private insurance coverage) of $1.75 million per claim.

All health care professionals contribute a yearly surcharge to pay for the fund, which is maintained at a minimum of $4.5 million. The surcharge demanded can be increased if the director decides more money is needed to pay all the claims made against the fund.

8) South Carolina Patient Compensation Fund

In South Carolina, the Patient Compensation Fund is available for qualified health care providers who join the fund by paying a yearly fee for membership. In addition, some health care providers may need to pay additional amounts, as determined by the Board of Governors. Doctors also need to carry insurance coverage of a minimum of $600,000 per aggregate or $200,000 per claim to qualify.

If a patient wants to bring about a general liability or medical malpractice claim, the patient needs to first file a notice of intent and must undergo mediation. The case itself is subject to evaluation for eligibility.

If a plaintiff is successful in their claim, the PCF will pay any awards over $100,000 per claim or $300,000 annually for participating medical professionals. The PCF is held separate from the state budget by the State Treasurer.

9) New York Excess Coverage Fund

New York’s Excess Coverage Fund is unique because it is paid by tax dollars rather than by surcharges. Hospitals offer the coverage to physicians with hospital privileges, and hospitals are then compensated by a state fund that is designed to pay for the PCF and other health care services.

The PCF in New York demands doctors have a minimum coverage of $3.9 million in aggregate or $1.3 million per case and must have secured hospital privileges. The fund offers an extra $3 million in the aggregate and $1 million per case in coverage.

In addition to the states listed, Florida, Wyoming, and Oregon have inactive PCFs. Florida and Virginia have PCFs, but the funds apply only to claims involving malpractice in situations involving infants who have suffered specific types of injuries.

How Do Patient Compensation Funds Affect Physician Insurance?

When it comes to claims of medical malpractice, a patient compensation fund can protect a physician or medical professional in a number of ways:

- Medical malpractice claims need to be reviewed by an approved commission or body for legitimacy before damages are awarded (generally this approval process takes place before the case goes to court, thus discouraging non-meritorious claims).

- Some funds require meditation or an evaluation, reducing frivolous claims and thus potentially reducing insurance costs for medical practitioners.

- Funds pay for larger settlements and awards, thus reducing what insurance companies need to pay. In turn, physicians become lower risks for insurers, and insurance carriers can offer more competitive premium amounts since they do not have to fear larger claims.

- By taking over larger settlements and awards, PCFs may limit the financial liability doctors face.

- Caps may be placed on the awarded amounts patients receive, thus reducing liability.

- Some funds place a statute of limitation on claims, reducing doctor liability.

- Some funds reduce attorney fees or place limits on attorney fees, reducing financial incentive for malpractice claims and potentially reducing the number of frivolous claims.

- Essentially, Patient Compensation Funds — also known as excess liability funds or excess coverage funds — take on the financial burden of medical malpractice awards above a certain amount. For participating doctors, these funds can also help reduce insurance premium costs by making medical practitioners less risky for insurance carriers.

With a fund, insurance carriers know that awards above a certain amount will be covered by the fund, and the insurer will not be liable. This means insurance companies do not need to anticipate high awards and payouts, which means physicians can enjoy lower premiums. Medical practitioners who might struggle to find affordable coverage may be able to find it by becoming part of a fund.

Many funds also discourage frivolous lawsuits by asking patients to submit intentions to file — usually with medical evidence — and by introducing meditation to the process. Without a fund, patients may primarily be communicating with a personal injury attorney about the possibility of filing a claim — and the attorney has a financial interest in pursuing claims. Patients in a state with a PCF are mediating with a committee or panel.

Patients may get needed information about the course of events leading to an injury when undergoing mediation, for instance. This may help reduce their interest in pursuing a legal action. The committee or panel evaluating the claim is generally made up of doctors who can determine the merits of a claim. The panel also does not have a vested financial interest in having the patient pursue a claim. Therefore, resolution may occur before the case even approaches the courts, reducing claims and the liability and legal actions physicians may need to face.

The Drawbacks of the Patient Compensation Fund

This is not to say that all experts believe PCFs are a solution for medical malpractice claims and high premium rates for doctors. Part of the criticism leveled against PCFs is that some states limit the total amount paid by the funds each year. If a patient is injured and the fund does not have enough assets to cover the amount, the patient may need to wait until money is available. In some states, larger awards are paid out over time. If a patient does not have adequate coverage due to these policies, however, they may seek other legal remedies.

Many state PCFs also require doctors to meet certain insurance coverage guidelines. In addition, most require doctors to pay surcharges — often a percentage of the insurance premiums doctors pay. These costs can be substantial and trying to ensure compliance to PCF rules can be a challenge at a busy professional practice.

State PCFs add an additional layer of complexity to a physician’s medical liability insurance program. Please reach out to your Gallagher Healthcare insurance professional for assistance in understanding and navigating the regulatory and licensure compliance requirements of practicing medicine in these states.

Contact Gallagher Healthcare for More Information

Gallagher Healthcare has extensive experience navigating the insurance environments in PCF states and specializes in custom multi-state medical malpractice insurance coverage. Contact Gallagher Healthcare today for a free consultation.

Post Updated 11/11/2016