The Data Behind Florida’s Supreme Court Decision

Gallagher Healthcare :: Industry Insights

By Trey Hutchins | 3/21/2014This will be the first installment in a series of blog posts that focus on state caps on malpractice insurance payments and the corresponding data. This is a hot topic in the industry right now, as the Florida Supreme Court recently overturned the cap in that state and there is a push to overturn MICRA in California, which has been used as the model in many other states, including Texas. This discussion will focus on Florida, since it is the most recent development; I will discuss other states in future posts. If there is a specific state that interests you, please email me and I’ll see if I can work it in to this series.

The case in Florida involves a woman who passed away shortly after childbirth (for details, see https://www.floridasupremecourt.org/content/download/242736/file/sc11-1148.pdf ). Justice Lewis spends a significant part of his opinion discussing whether there is or was a malpractice insurance crisis in Florida. This is very difficult to determine, as there are not perfect data available and the information that is available includes so many variables that it would be easy to construct multiple arguments both for and against either opinion.

It appears that the Florida Supreme Court looked at data and research from several different entities, including Weiss Ratings, Florida Office of Insurance Regulation, and others. I did not see any mention of data from the National Practitioners Data Bank (NPDB), which tracks malpractice claim payments by state. Let’s take a look at Florida using NPDB data for some key indicators, including:

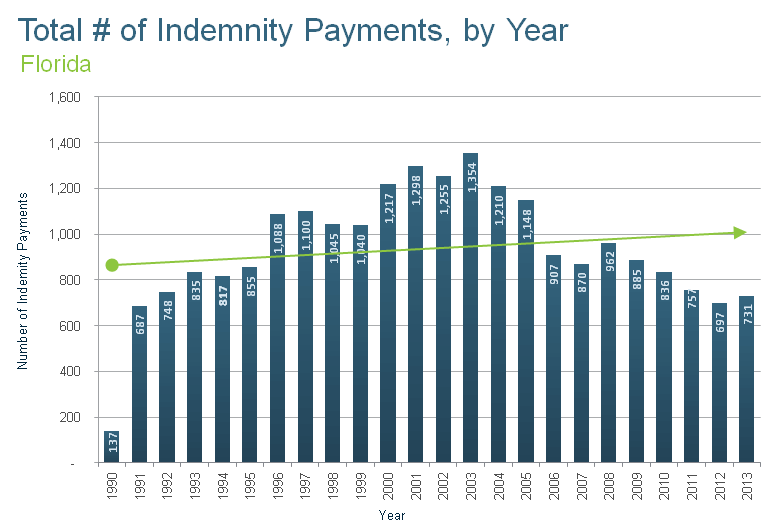

Total Claims Filed, by year, 1991–2013

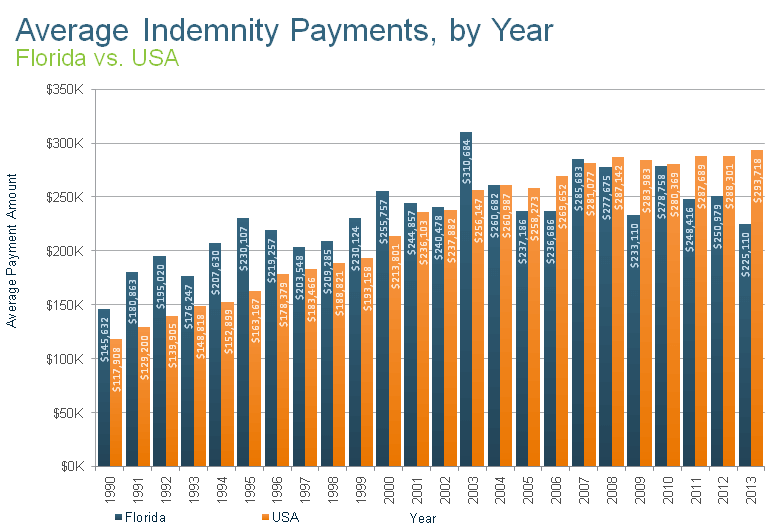

Average Indemnity Payment, compared to US average, 1991–2013

Keep in mind that carriers are only required to report payments, so there are no data on claims that were dropped, dismissed, or won by the defending physician.

As the largest broker for physicians in the US, Gallagher tracks this data to forecast the market and educate our clients. For a quick overview of the malpractice insurance environment in Florida please visit our state summary page.

According to the most recent databank report (see chart above), Florida had 731 malpractice insurance payments in 2013. This is down significantly from the high of 1,354 claims in 2003 (a reduction of almost 50%). In fact, Florida has seen fewer claims almost every year since 2003. Therefore, it’s reasonable to say that Florida’s tort reform (caps on medmal payments) seems to be working. True, we’re looking at number of claims filed and the tort reform merely limited what can be paid out, but the industry thinking is that taking out the “lottery” effect—removing the possibility of enormous settlements and judgments—makes plaintiff attorneys much more selective about the cases they take.

The data on average indemnity payouts follows a similar trend. The average indemnity payment in Florida for 2003 was $310,684, the highest it has ever been. While the average payout has fluctuated over the past ten years, it has been under $300,000 throughout that time frame. If anything, payments in Florida appear to have stabilized while the rest of the US has continued to see increases. The average indemnity payout in Florida was above the US average from 1990 to 2003; it has been below the average in nine of ten years since 2003. In fact, from 1990 to 2000, the average indemnity payment in Florida was significantly higher than the US average, with a large spike in 2003. While the change is not is obvious as it is for the number of claims, this data still seems to show that the damage caps enacted in Florida have reduced the amount paid out in malpractice indemnity payments.

Now let’s look at it from a dollar value: in 2003, there were 1,354 claims payments for an average of $310,684, meaning that $420,666,136 was paid out in malpractice payments in 2003. Last year (2013), there were 731 payments averaging $225,110, for a total of $164,555,410— a reduction of over $256 million dollars, or more than 40%. Given that plaintiff’s attorneys usually take about a third of a settlement, the cap cost them $85 million in 2013, and probably more, since both number of claims and average indemnity payments would have very likely continued to increase without the cap.

While I am not going to argue whether there was an actual malpractice crisis in Florida, I think there are several possible conclusions to be determined from this data:

- Prior to the damage caps, Florida was a higher-risk state than average for medical malpractice claims, compared to the rest of the US.

- The passage of damage caps reduced both the number of malpractice insurance claims filed and average indemnity payments.

- The passage of damage caps has moved Florida from one of the higher-risk venues in the US to one that is considered less risky.

The real question now is, how will the removal of claims limits for death cases affect claims over the next ten years? In a future post, we’ll review what has happened in a few states that have overturned damage caps to see if we can find any trends.