Common Medical Malpractice Insurance Policy Forms

Updated March, 2019

The general public is familiar with the idea of insurance. People have insurance for their cars, their homes, their boats and more. The idea behind insurance is that a lot of people who have a certain kind of risk in common — people who drive cars for instance — share that risk. While it's difficult to predict the risk for a single individual, insurance experts can look at a large group of people and predict the possible outcome.

The group of people with the same type of risk pay insurance companies premiums. The insurance companies determine how much the premiums will be based on predicted outcomes. In exchange, the insurance company will provide monetary compensation to policyholders paying the premiums if an insured event happens. By paying the insurance company a small amount up front to assume the risk, individuals can avoid financial ruin.

Insurance specifically for medical practitioners including surgeons and physicians is called medical professional liability (MPL) insurance. If a patient or their family claims medical negligence or files a medical malpractice lawsuit, this insurance protects medical workers financially.

So when a large group of people shares that risk, they pay less to protect themselves than they would if they were doing it on their own, and it is easier for the company that assumes that risk to pay financial compensation in the event of an accident. In other words, you pay a smaller amount up front in exchange for being protected from financial ruin in the case of an accident.

Medical Malpractice Insurance Definition

What works for people who want to protect their cars or their homes also works for people who work in healthcare industries. Medical malpractice insurance shares the risk of a lawsuit among many people who have the same kind of risk. If a patient or a group accuses a healthcare worker of negligence and files a lawsuit against them, medical malpractice insurance provides financial coverage for items including attorneys' fees, court costs and, in the case of that healthcare professional being found guilty of negligence, payments for a settlement or judgment if the healthcare worker settles out of court or is found guilty.

For a lawsuit to proceed as a medical malpractice case, it must fulfill four different criteria:

- The medical provider must have a duty to the patient

- The medical provider breached that duty as a result of action or inaction

- An injury resulted from the breach in duty

- There must be an established link between the injury and the medical provider

All four of these elements must be present for a medical malpractice lawsuit to be warranted. If even one of these criteria is not met, there is no established case for medical malpractice. Medical malpractice lawsuits are incredibly complex and very expensive. Because these cases have large payments at stake, both the defense and the plaintiff will aggressively pursue a judgment in their favor. Fortunately for doctors, many of these claims are "frivolous" because they do not meet the four above criteria, and are dismissed or won at trial.

If doctors and healthcare workers were required to pay these costs on their own, there would be far fewer people working in medical fields for fear of financial ruin. When they purchase medical malpractice insurance, healthcare providers can pool the risk in several ways, ensuring that if an accident does happen, they do not face financial disaster.

What Does Medical Malpractice Insurance Cover?

Basically, malpractice insurance covers allegations of negligence. It protects the physician if a patient alleges that the physician failed to provide them with the proper treatment, made a mistake during the treatment or omitted an important part of the treatment.

Some state laws require physicians and other healthcare workers have medical malpractice insurance. Other states, however, do not require it. Some physicians have decided to "go bare"or not purchase medical malpractice insurance. While this is legal, it is not advisable.

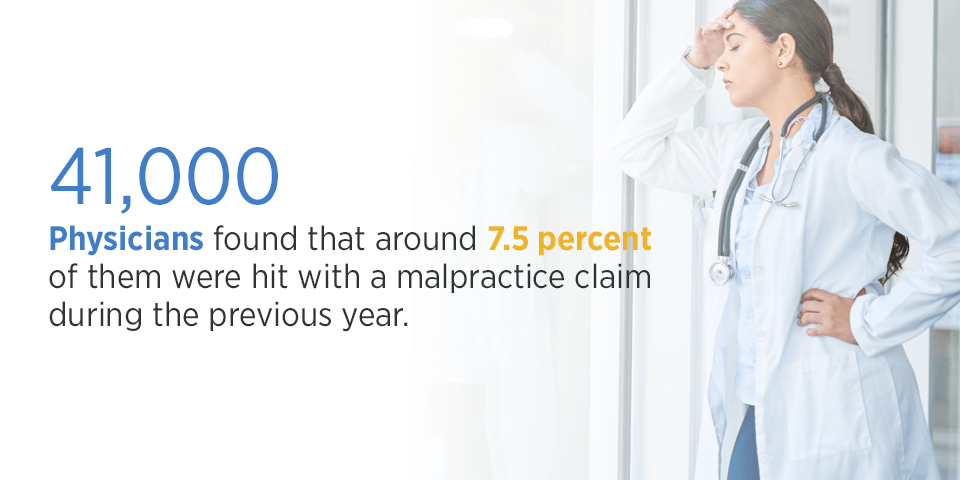

A study published in the New England Journal of Medicine in 2011 that surveyed almost 41,000 physicians found that around 7.5 percent of them were hit with a malpractice claim during the previous year. The study also found that for physicians in low-risk specialties — such as internal medicine — roughly 75 percent of them will be the subject of a malpractice claim at least once by the time they reached age 65, and almost 20 percent of them would need to pay for a settlement or a judgment.

The figures were even worse for physicians who work in high-risk categories, such as neurosurgeons. Almost every physician in a high-risk specialty will be sued at least once by the time they reach age 65, and 71 percent of them will lose their cases and make a settlement or a judgment payment.

With the average payout about $353,000 between 2009 and 2014, you can see why physicians need medical malpractice insurance, even in states where it is not required.

Who Needs Malpractice Insurance?

Anyone who works in the healthcare field needs to purchase medical malpractice insurance.

1. Hospitals

Hospitals need medical malpractice insurance as well. When hospitals purchase insurance, it is known as hospital professional liability (HPL) insurance. Larger hospitals or those that are a part of a coordinated system are increasingly self-insuring some or all of their risk. They can do this because of the size of the hospital. The hospitals will insure many of the doctors and healthcare providers who work there.

Other facilities will require malpractice insurance including long-care facilities, behavioral health centers and same-day surgery facilities. Premiums for these facilities will depend upon their location, the procedures the facility provides and the specialties of the doctors who work there.

2. Group Practices

A group practice will buy insurance under a group policy. This negates the need for physicians or healthcare workers in the practice to buy their own insurance. A group insurance plan saves money and can be customized to fit the needs of each particular group practice.

3. Medical Students

It's unlikely that a medical student will be named in a lawsuit but there are some exceptions. Normally the institution where the student trains will cover their insurance needs. But if they are on a fellowship or doing advanced studies at a different institution than the one where they are a resident, then they are not covered.

4. Podiatrists

Although they only work on feet and ankles, podiatrists are physicians. They are increasingly in demand to treat ailments such as diabetes. While medical malpractice insurance for podiatrists normally costs less than other physicians, podiatrists can still be the subject of allegations of malpractice and so need insurance to protect them.

5. Physician Assistants

Since physician assistants work in a wide range of situations and, depending upon the state where they work, have varying degrees of independence, the insurance they need will depend upon their situation.

6. Nurses

Anyone who works as a nurse, be it as a registered nurse (RNs), a nurse practitioner (NPs) or a certified registered nurse anesthetist (CRNAs), needs insurance. The cost of insurance for registered nurses is relatively low, depending upon the state where they work. Premiums for nurses who work in more specialized areas are more variable and often depend on any past claims against them as well as the state.

7. Physicians

There's no way to avoid it. Doctors need medical malpractice insurance. There is a financial risk involved in not having any insurance, not to mention that many hospitals will not allow doctors to have staff privileges without having malpractice insurance, even in states where it is not required.

Types of Medical Malpractice Carriers

A variety of companies provide malpractice insurance, with each company offering advantages and disadvantages. No one company is a one-size-fits-all for every kind of physician. Depending on the physician's location and their specialty, doctors may be required to use one type of company or have a choice about which one best fits their needs.

1. Admitted Carriers

The most common type of MPL insurers are admitted carriers. These companies are structured according to state guidelines and are regulated by the state Department of Insurance. All rates and policies must be approved by the Department of Insurance before an admitted carrier can use them. These carriers are also backed by a state guarantee fund, which provides an extra layer of coverage in the event that the insurance company becomes insolvent.

2. Excess and Surplus Lines

Many insurance companies write medical malpractice insurance in the Excess and Surplus Lines market. These types of companies are not admitted or regulated by the state. This allows them to craft their policies and rates for particular risks. Often, this type of carrier insures hospitals due to their need for large limits of liability. Doctors who work in high-risk areas also frequently choose these companies. Although they are not regulated by their state Department of Insurance, which means that they are not a part of the state guarantee fund, these companies still must be approved before they can be used by physicians in a state.

3. Risk Retention Groups

Risk Retention Groups (RRGs) operate much like mutual companies. They are owned by the policyholders which they also insure. These groups are not admitted carriers so they can avoid many state regulations and red tape. Lowering the cost of premiums to the doctors that participate in them is the primary goal of most RRGs. If there are surplus funds at the end of the year, many risk retention groups even offer dividends back to the shareholders or put the surplus back into the company and lower the cost of premiums.

4. Captives

A captive insurance company is created when an insured's risk is large enough, and is diversified to the point where they can become self-insured. This usually occurs with large entities, like hospitals, who have enough capital to be able to self-insure.

5. Trusts

Some states allow physicians to create a trust to insure its members. These trusts are subject to different regulations than admitted carriers but are reviewed to varying degrees by the Department of Insurance according which state they are in.

6. Joint Underwriting Associations

Joint Underwriting Associations (JUAs) are to some degree the last resort for physicians who work in hard-to-insure specialties or who have had many claims made against them in the past. This type of company is used when there is difficulty finding coverage in the normal market. As an insurance company which is run by the state, it is often the last resort for physicians who are not able to obtain coverage elsewhere.

When you choose an insurance company, consider the different types of carriers available and which one you think would be the best fit for your practice. It is in your best interest to talk to a medical malpractice insurance professional who can help you determine what type of insurance is right for your needs.

Types of Policies

Within the medical professional liability world, there are two main types of policies — claims-made policies and occurrence policies. An occurrence policy is the same type of policy carried for a car or a home. These policies assign payment of a claim to when it occurred. If you had a car accident in 2009, the 2009 insurance policy would cover the claim. Claims-made policies are based upon when the claim is filed, not when the incident occurred. Using the car accident as an example, if the claim was filed in 2009, the 2009 policy would cover it. However, if the claim was not made until 2011, the 2011 policy would handle the claim even if the accident happened in 2009. Deciding which type of policy is best for a physician's situation is often one of the most confusing aspects of MPL insurance.

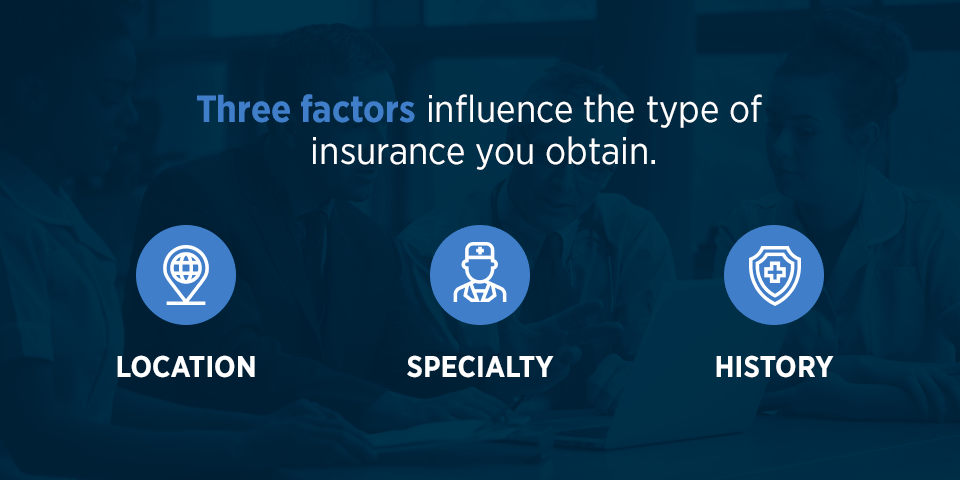

Three factors influence the type of insurance you obtain:

- Location:Different states have different malpractice insurance requirements and rates. A surgeon operating in Iowa or Montana is going to pay a lot less in medical malpractice insurance premiums than a doctor who practices in Brooklyn, N.Y., or Washington, D.C.

- Specialty:The type of medicine you practice will also help determine the kind of insurance you need. Someone who practices internal medicine will pay a much lower premium than a neurosurgeon or bariatric physician.

- Loss history:As already noted above in the New England Journal of Medicine study, most doctors can assume they will be the subject of a medical malpractice claim at least once before they turn 65. If you had very few or no claims against you in the past, your insurance premiums will be lower. If, however, you had a history of claims being made against you, your rates will be higher.

Aside from the different kinds of medical malpractice insurance you can purchase, you can also purchase your insurance from a single company or use an independent insurance broker who will look at a variety of companies and policies to find you the best one.

Here is a bit more detail about each type of policy:

1. Claims-Made

This is the most popular kind of medical malpractice insurance. With the claims-made policy, the insurance company will provide coverage only for a claim made during the period when the policy is in effect. If a claim is made against a physician after that physician has canceled a claims-made policy, that physician is liable for the claim and would no longer be covered by the policy, even if the incident that provoked the claim happened when the policy was in effect. Physicians who leave claims-made policies need to purchase a kind of coverage known as tail malpractice or extended reporting coverage.

2. Occurrence

Occurrence policies provide coverage for a healthcare provider while the policy is in effect even if the claim happened before the term of the policy. These policies are considerably more expensive than claims-made policies but when you cancel an occurrence policy, you do not need tail coverage afterward. Only a few insurance companies offer occurrence policies because of the difficulty of predicting how many claims may be made against a physician in the future based on services provided in the present day.

3. Claims-Paid

The premiums for these policies are determined by the number of claims that were paid during the previous year, as well as any claims that are anticipated to be paid in the future. Claims-pay policies can be assessable — meaning that the policyholder could be charged extra above and beyond the initial premium to cover an insurer's unexpected losses if the original premium does not cover the funds paid out in a settlement or judgment. These policies may be assessable for a limited time or indefinitely. Claims-paid policies are relatively rare in the medical malpractice insurance industry and are not offered in most states.

4. Tail Coverage

Tail or extended reporting coverage offers protection for physicians who have canceled a claims-made or a claims-paid policy. As noted above, when a healthcare provider cancels a claims-made or claims-paid policy, they are not covered for an incident that happened when the claims policy was in effect. Tail coverage provides a solution to this dilemma by providing coverage for claims resulting from an incident that occurred when the policy was in effect — which makes it somewhat like an occurrence policy. A physician typically purchases tail coverage insurance from the company which owns the now-canceled claims-made policy.

They are expensive — normally about 200 percent or more of the last premium that the physician or healthcare provider paid when their claims-made policy was in effect — but they are very popular and are widely available from insurance companies.

5. Nose Coverage

Nose or retroactive coverage lets you move your retroactive date to a new insurance carrier. It is similar to tail coverage only instead of buying coverage for incidents that happened in the past from the previous company, you purchase it from your new company which provides current coverage. In most cases, nose coverage is less expensive than tail coverage.

It is critical that physicians and healthcare providers are aware of their retroactive date. It is the day that you started being insured under a claims-made policy.

For more information on claims-made and occurrence policies please refer to our claims-made vs. occurrence discussion.

Policy Components

Policies have different components that are important for physicians and healthcare providers to understand. Not understanding how your policy works can have detrimental outcomes.

1. Consent to Settle

Some professional liability policies provide that the insurer is allowed to settle a claim without the consent of the insured. Others provide that the insured has the right to veto a proposed settlement by the insurer. Since a settlement can affect the reputation and earning ability of the insured, this type of clause is an important consideration in selecting a policy. None means the insurer is allowed to settle a claim without the consent of the insured. Yes means the insured has the right to veto a proposed settlement by the insurer.

If a claim is made against you, you may feel that you are innocent and that, if you take the claim to trial, you will prevail. The insurance company, however, may feel it is in their best interests financially to settle the claim before a court case. This policy can have long-lasting effects on a physician's reputation and also on the premiums they will pay in the future.

2. Hammer Clause

Sometimes an insurance company will include a provision known as a hammer clause under a consent-to-settle clause. This is because the insurance company wants to encourage the policyholder to accept their recommendation of a settlement. This clause states that if the insurer recommends a settlement offer, but the insured refuses the offer, the insurer is only liable for the amount of the settlement offer.

For example, if the insurance company recommends a settlement offer of $60,000, and the doctor vetoes the settlement, but ultimately the doctor must pay an $80,000 judgment, the insurance company is liable only for the $60,000 of the original settlement offer. The doctor would be responsible for the remaining $20,000 plus any deductible.

3. Coverage Trigger — The Claims-Made Requirement

For a policyholder to receive coverage from a claim, that claim must be made to the insurance company during the period the claims-made policy is in effect unless the physician has purchased tail coverage. So it is important for a physician purchasing insurance to scrutinize the language around the requirement that activates coverage.

This requirement to activate coverage may create a significant challenge because determining the exact time when a claim is made is not always simple. Policies often contain a definition of claim, and the definition can vary significantly from one contract to another. With one policy, a verbal allegation may be enough to meet the definition of a claim, while another contract will require a written demand for money or services. Two common examples of claim definitions are written demand and incident trigger.

4. Written Demand

This type of claim is constituted by any written demand from a person or organization that it is the intention of the person or organization to hold the insured responsible for the results of a specified wrongful act.

5. Incident Trigger

An incident trigger allows both written demands claims and any incident which the policyholder expects will turn into a claim at a later date even though a written demand has not been made yet.

6. Defense Costs

There are two types of defense costs — inside and outside:

- Inside:These policies are also called "self-liquidating," "self-consuming," "defense within limits," or "wasting" policies since any money spent on defense is no longer available to pay a judgment or settlement. If an inside policy has $1 million coverage, but defense costs $1 million, the policy is completely liquidated, even if litigation is still in progress.

- Outside:More expensive than inside policies, insurance companies pay all defense costs including any costs of an attorney who is selected by the company. The limits of your policy are not reduced by payment of defense costs.

7. Locum Tenens

If a physician is away from the practice because of a conference or on a vacation, this policy covers the temporary physician who takes the place of the policyholder or member of a medical group. This policy may be dependent on the main policyholder not practicing medicine while the Locum Tenens policy is in effect.

8. Punitive Damages (Exemplary Damages)

Punitive or exemplary damages in addition to and separate from the compensatory damages a plaintiff receives. Punitive damages are meant to be a punishment for the defendant.

9. Guarantee Funds

In the case of admitted carriers, the policy will be backed by a state guarantee fund. If the insurance company becomes insolvent, the guarantee fund will cover claims for a period of time as determined by the state.

10.Notice of Non-Renewal

Many states require insurance companies to provide policyholders with written notice well in advance of their intentions to cancel or not renew a policy. Although most states mandate a minimum number of days that are required to give this notification, most insurance companies will provide a longer window. This allows the policyholder to look for a new policy with a different company. The policyholder can then put his new policy in effect before the end of the old policy. This is important because it is often difficult to purchase a new policy when a physician has had a policy canceled in the past.

11. Portability

This allows healthcare providers to take their current policy with them when they need to move to another state without having to purchase any tail coverage. Since many insurance companies don't operate in all 50 states, it's important for the healthcare provider to investigate the portability of their coverage. If the insurance company does not operate in the state to which the healthcare provider is moving, they may need to purchase tail coverage. If you know that you may be moving at some point in the future to a new state, purchase coverage from a company that operates both in your old and new location.

12. Discounts and Credits

Companies that ensure your car often offer drivers reduce premiums if they take specialized driver ed courses or have no accidents on their record. Medical malpractice insurance companies often offer similar discounts and credits. If a physician takes a course in risk management, joins a professional association, has no recent record of claims, is part-time or has just started the practice, insurance companies often use these kinds of discounts to entice physicians to use their products. These discounts can often be quite substantial, so it's important for physicians and healthcare providers to consider them when they are choosing a medical malpractice insurance company.

Where Do I Buy Medical Malpractice Insurance?

Malpractice insurance policies are sold in one of three ways. All three methods provide coverage and customer services, but there are essential differences between the three:

- Direct writers: These are companies that sell their policies directly to physicians and other healthcare providers. They use their own agents and producers, and any customer service functions are carried out by the company's own staff.

- Captive agents: An insurance company will hire independent insurance agents to promote and sell only their company's product. Captive agents are not permitted to represent other companies. Customer service functions, however, are provided by the agent and anyone who works for them.

- Independent agents: Independent agents work with several malpractice insurance companies. They sell and market the products of all the companies with which they work. Like captive agents, they also provide all customer service options for policyholders. But unlike direct writers or captive agents, independent agents can provide many options to a physician looking for a policy. This often allows the physician to purchase insurance at a better rate and find coverage options that are more appropriate for them.

Physicians or healthcare providers do not need to pay independent agents anything for their services. The commissions they receive from the insurance companies with whom they do business is already included in all premiums.

Malpractice Insurance Rates

As we noted above, three factors can affect the rate a medical provider pays for MPL.

Insurance rates are determined by the risk factors associated with the doctor's specialty, the location in which the physician practices, and the physician's claims history. Some specialties traditionally have a higher severity and frequency of indemnity payments than others. For example, a neurosurgeon has a greater risk for a high paying malpractice claim than a pediatrician does. The greater the risk associated with each specialty indicates a higher insurance rate for that type of physician.

Location is also a large factor in determining insurance rates. Insurance companies collect claims information to determine trends within states and counties. Holding all other factors constant, an OBGYN practicing in Omaha, Neb., will have a much lower rate than if he was an OBGYN practicing in Manhattan, N.Y.

The third variable which influences insurance rates is "loss history." This is the record of lawsuits in which a physician has been named as a defendant, regardless of whether the claim was dismissed, settled or paid out as a result of a judgment. Obviously, a doctor who has had five claims in the past two years will receive a higher rate than a physician who has never had a claim.

While these three variables — specialty, location and loss history — are relatively straightforward, the process of determining rates is complicated by the very nature of insurance — predicting future losses. Looking into the past, it is easy to say what the rates should have been, but looking into the future makes it a little more complex. The insurance companies must rely on predictive models as well as past claims trends in an attempt to set appropriate rates. Often carriers will contract with actuarial companies or employ actuaries within their company to develop and use these complex models.

Is Malpractice Insurance Tax Deductible?

Yes, medical malpractice insurance is tax-deductible. The IRS allows medical malpractice insurance premiums to be deducted as a miscellaneous itemized deduction. However, it would be in your best interests to consult with a tax professional who can advise you on how you take advantage of any tax benefits.

Factors That Affect the Cost of Medical Malpractice Insurance

Along with location, specialty and history with claims or losses, several other factors determine how much medical malpractice insurance will cost a physician or healthcare provider.

- Hours the physician works :The longer you work, the higher your risk. The more patients a physician or a healthcare provider sees, the greater the possibility of a mistake or an omission. Long hours can sometimes be connected to unforeseen circumstances. Overworked and tired doctors are more inclined to make mistakes. Physicians who work a limited number of hours in a week are more likely to see lower premiums.

- Competition: When there are two gas stations on one corner, there is a likelihood that they will get into a price war. With malpractice insurance, the more companies that work in a state, the greater the competition. As a result, some of these companies will occasionally go to the Department of Insurance in that state and ask to lower the rates to be more competitive.

- Tort reform: In the latter half of the 20th-century, the number of malpractice lawsuits against physicians exploded. Physicians were paying enormous sums of money to settle claims or judgments. As a result, 33 states have instituted tort reforms that address the rising cost of medical malpractice insurance and what plaintiffs can reasonably pursue. Caps on non-economic damages, in particular, have played a significant role in gradually lowering the amount of money that is paid out every year in settlements and judgments for malpractice claims.

- Policy limits: Policy limits work in two ways. They are usually split. If a physician has a $1 million/$3 million limit, that means the insurance company will pay up to $1 million on each claim and $3 million during the life of the policy. The higher the limit, the larger the premiums, but the more protection offered.

- Defensive medicine: This is often cited as one of the main reasons for the rising cost of healthcare, which may or may not be true. Many doctors worry about being the subject of a malpractice claim and overprescribe the treatment for a patient. They may order extra diagnostic tests or surgery when it's not needed or put a patient in the hospital to avoid the possibility of a legal claim. Defensive medicine, however, can work against the physician and result in larger premiums. The more tests a doctor gives and the more surgeries they order, the greater the chance they will make an error. Plus, as we noted above, the more hours a doctor works, the higher the premium is likely to be.

- Variances in practices: If a doctor works across state lines or in multiple facilities, they could find that their premiums increase.

Going "Bare"

As states have made meaningful tort reforms, it has become affordable for more physicians to purchase malpractice insurance. Yet some doctors have decided not to carry it or to "go bare." The main reason doctors go bare is they think if they don't have medical malpractice insurance, it is less likely they will be the target of a lawsuit. They believe that if the plaintiff's attorney discovers they do not have malpractice insurance, the lawyer is less likely to recommend to the plaintiff to go ahead with the suit.

This is a mistake, however, as it may work in some limited situations, but plaintiff's attorneys can still go after the assets of the physician or their business. Going bare is truly a roll of the dice. It does not guarantee that a physician will never be the target of a malpractice claim or ever need to pay a settlement or judgment.

About 60 to 65 percent of all claims made against physicians are dismissed or dropped. The downside to this, however, is that this often does not happen until after the legal action has already begun. So even if the doctor doesn't have to pay a settlement or claim, they will still have to pay for the services of a lawyer to defend them against the claim or the lawsuit until it is dropped.

Additionally, some states require that a physician carry malpractice insurance, and many hospitals will not give a doctor staff privileges without the doctor having medical malpractice insurance.

What Will You Need When You Apply for Malpractice Insurance?

While each insurance company has different requirements for what is needed before you can purchase a medical malpractice insurance policy, it is generally useful to provide the following items:

- The complete application for the policy

- Letterhead from your individual practice or from the group or hospital where you practice

- An updated copy of your CV

- A copy of your DEA license

- The Declaration Page — usually the first page — of your past or current policy

- A copy of the advertisement which may have brought the company to your attention, if available

- The reports of all the claims that have been made against you and all the payouts you've had to make for the past 10 years

Don't try to hide anything — be as truthful as possible. If you fail to report a claim made against you in the past, the insurance company might raise your premiums or cancel your policy.

A Short History of Medical Malpractice Insurance

The first instance of a patient making a complaint against the physician for malpractice was almost 700 years ago, although it probably happened even sooner in the Islamic world during its golden age. In 1374, Agnes of Stratton filed a lawsuit against a London-based surgeon named John Swanlord. Dr. Swanlord said he would treat Agnes' mangled hand, but she was not happy with the outcome and sued for breach of contract.

Believe it or not, this case set an important precedent that is still in effect almost 700 years later. Chief Justice John Cavendish of the Court of King's Bench ruled that a physician can only be held responsible if the plaintiff was harmed as a result of an act of negligence. Treating the disease or injury an appropriate way but not being able to completely heal it or cure it did not rise to the level of negligence.

Medical malpractice remained relatively uncommon for centuries but then in the mid-1800s in the United States, malpractice insurance claims skyrocketed, rising by 950 percent. Why the sudden increase? As the United States began to grow, improvements in transportation and communications, as well as changes in culture and the practice of medicine, may have played a role.

In the early 20th century, many doctors became members of state medical societies. At least one of these societies, the Massachusetts Medical Society, offered malpractice insurance as an inducement to join its group.

Malpractice insurance claims increased again in the late second half of the 20th century. California created one of the most important responses to this when it passed the Medical Insurance Comprehension Reform Act (MICRA) of 1975.

It provided caps on non-economic damages and attorneys' fees, introduced the idea of binding arbitration and reduced the amount of time a plaintiff had to file a claim. It also allowed physicians to pay a claim or judgment over time. MICRA became a model used in many other states and is believed to have reduced the liability of healthcare providers by around 30 percent.

Let Gallagher Help You With Medical Malpractice Insurance for Yourself, Your Group Practice or Your Hospital

Gallagher Healthcare is a large national broker of medical malpractice insurance. Unlike an insurance agent who represents a specific insurance company, a broker acts solely on behalf of the physician. Gallagher brokers can advise healthcare providers on the ins and outs of the market, explain confusing policy language, and negotiate the best policy coverage and rates on behalf of their clients. By using Gallagher to find insurance, physicians can stop worrying about the headaches of medical malpractice insurance and can concentrate on their patients. The following are just some of the many reasons to partner with Gallagher Healthcare in finding medical malpractice insurance:

- We have active relationships with all types of insurance companies, and can advise which type of insurance carrier best fits the physician's situation;

- There is absolutely no cost to you for utilizing our services – We are paid via a commission from the insurer that is built into their rates regardless if you choose to utilize a broker;

- Without broker assistance, a physician is limited in negotiating favorable terms and conditions – Our experts can quickly outline all available options, and ensure the practice is getting the best terms possible;

- We are the largest provider of insurance products to physicians nationally, bringing unmatched leverage to market relationships;

- We are part of the Gallagher family, recently named the top Ethical Insurance Broker in the U.S.;

- We can be your "one stop shop" for all your insurance needs, ranging from employee benefits to general business insurance, as part of the Gallagher team;

- We are the best in the business within our specialty – Physicians Malpractice Insurance.

You can learn more about us and the services we provide or request a quote and a member of our team will get back to you as soon as possible.

References

- The American Medical Association. https://www.ama-assn.org/about/publications-newsletters/alexa-flash-briefing-news-ama

- Texas Department of Insurance. http://www.tdi.texas.gov.

Premium savings is just one click away! Complete this form to receive your FREE, NO OBLIGATION medical malpractice insurance quote. You can also call us at 800.634.9513 and ask to speak to a salesperson.