California Medical Malpractice Insurance

Before the passage of the Medical Injury Compensation Reform Act of 1975 (MICRA), California faced a medical malpractice insurance crisis. Fortunately, since MICRA was established, California has become one of America's most stable medical malpractice markets.

Today, you'll find numerous companies that offer medical malpractice insurance, though navigating the market can sometimes feel overwhelming. You're bound to have lots of questions. How much does medical malpractice insurance cost in California? Are you required to carry malpractice insurance in California? How much malpractice insurance do you need?

Medical malpractice insurance is crucial for a successful medical career. That's why we've compiled this guide to what you need to know about this essential coverage.

California Medical Malpractice Fast Facts

Though you may want to solicit advice from an insurance professional that's specific to your situation, including your location and specialty, we've gathered some general facts about medical malpractice insurance in California to get you started.

1. Are You Required to Carry Malpractice Insurance in California?

In the state of California, physicians are not required to carry malpractice insurance. Even though malpractice insurance isn't required in California, physicians may still want to obtain this coverage.

You may find that a hospital or another facility requires its visiting providers to have malpractice insurance. To participate in certain healthcare insurance plans, you may also be required to have malpractice insurance. While there is a cap in California on non-economic damages at $250,000, there isn't a cap for lost wages. This means doctors who are successfully sued could pay hundreds of thousands of dollars in damages. Add legal fees on top of that, and you're dealing with a hefty bill.

Overall, malpractice insurance can prevent a large financial loss for physicians in the event of a lawsuit.

2. How Much Malpractice Insurance Do I Need in California?

How much malpractice insurance you need in California will depend on your location and specialty. For example, if you're a surgeon, you'll likely need more coverage than doctors who don't perform operations, since the risk is greater for your patients.

To determine how much insurance you need, you should also decide whether you need an occurrence or claims-made policy and if you should add on nose or tail coverage.

- Occurrence policy: This policy covers incidents that occur during the active period of the coverage. Say your occurrence policy expired a year ago, and now someone has brought a suit against you for an incident that occurred during the time you were covered by the occurrence policy. Your cost will be covered by this insurance.

- Claims-made policy: This policy is essentially the opposite, as the only claims that are covered are those that are made while you're carrying the policy. If a suit is filed against you after your coverage has expired, you won't have insurance to cover the lawsuit.

The benefit of a claims-made policy is that the premium is typically lower than for an occurrence policy, particularly in the early years of the physician's practice, since the potential for a claim increases gradually.

To avoid being without coverage after a claims-made policy expires, you can purchase nose coverage on a new insurance policy or a tail policy.

- Tail policy: This coverage can be obtained after you cancel your policy or after you leave a practice. With a tail policy, you'll have extra time to report claims after your malpractice insurance policy ends. You may want a tail policy if you're changing to a new type of policy, if you're retiring from the medical practice or if your new insurance carrier doesn't include prior acts coverage.

- Nose coverage: This coverage can protect you for incidents that happen before you have a policy in place. This may also be known as "prior acts" on a new policy, providing retroactive coverage that covers you back to a specific date. If you don't want a tail policy, you may want to consider this alternative.

If you're unsure what exact coverage options are best for you, you can speak with an insurance provider about your specific situation.

3. How Much Are California Medical Malpractice Insurance Rates?

The insurance rates you can expect depend on your county and specialty, along with your history of malpractice claims. If your specialty is high-risk, then you may want to obtain more than the minimum coverage. For example, insurance premiums for obstetricians/gynecologists in California were under $50,000, while in some counties of New York, premiums were nearly $215,000.

Tort Reform in California

The medical malpractice insurance crisis arose when juries began awarding extreme financial compensation, causing medical malpractice premiums to skyrocket by more than 300%. Most notably, MICRA placed a $250,000 cap on non-economic damages (i.e. pain and suffering) only and did not cap damages for lost wages, medical bills, among other measurables. MICRA also places a cap on the plaintiff attorney fees on a sliding scale basis.

While the constitutionality of MICRA has been challenged numerous times (mostly in the late 1970s and 1980s), revisions to the law have been proposed to the California electorate twice since 1975, once in 1999 and again in 2014. Both proposed revisions sought to adjust the $250,000 non-economic damage cap to better reflect either the current cost of living and/or the inflation that has occurred since its passage. In 1999, a California bill sought to increase the $250,000 cap to reflect the cost of living. To maintain the current cap in 1975 dollars, the cap would increase to $753,000 by the year 2000, according to the 1999 bill. However, this bill was not passed, and the current cap on non-economic damages remained at $250,000.

The 2014 proposition was deemed California Proposition 46, the Medical Malpractice Lawsuits Cap and Drug Testing of Doctors Initiative. Proposition 46 made it onto the November 2014 California ballot. Its purposes were the following:

- To peg the non-economic damage cap to inflation which would effectively increase the cap from $250,000 to approximately $1.1MM

- To require drug and alcohol testing of physicians and mandate reporting positive results to the California Medical Board

- To require the California Medical Board to suspend the license of any physician with positive alcohol and/or drug test results

- To require all healthcare providers to report another provider suspected of being under the influence of drugs or alcohol or suspected of medical negligence

- To require all providers to consult the California prescription drug database prior to issuing prescriptions for controlled substances

Proposition 46 was defeated, with 67% of voters against the legislation and 33% voting in support. If Proposition 46 passed, it would have been the first law in the nation requiring random drug and alcohol testing of physicians.

Since MICRA was established in 1975, California has become one of the most stable medical malpractice markets in the country. MICRA has served as the national model for state and federal liability reform efforts.

Claims Trends and Analysis in California

Claims-made policies are the most common policy type in California, premiums start lower in the first year, but will rise as you continue to practice and accumulate years, often reaching a mature rate five to six years after initiating the policy. Claims-made coverage provides coverage for claims that arise while the policy is in effect if the insured had coverage at the time of the incident.

Statute of Limitations

The statute of limitations in California for medical malpractice is three years after the injury occurred or one year after the discovery of the injury. There are some exceptions to this timeline, however, when it comes to minors.

California's official statute specifies that a medical malpractice lawsuit must be commenced on behalf of the child within three years of the occurrence of the alleged malpractice. If the child is under six years old, the medical malpractice lawsuit must be filed within three years of the date of the alleged malpractice or prior to the eighth birthday of the child. This stipulation depends on whichever is the larger timeline.

Liability Limit

The typical limits of liability in this state are $1MM per occurrence with a $3MM aggregate limit. Most hospitals require their doctors to carry these same limits of liability.

Insurance Companies in California

Many factors are taken into consideration when determining which carrier to choose. Such factors include AM Best rating, the year the company was founded, coverage trigger and free tail provisions. There are three types of medical malpractice insurance carriers in the state, including Stated Admitted Carriers, Surplus Lines Carriers and Risk Retention Groups. Over the past few years, fewer claims have been filed, allowing some carriers to pay dividends and offer rate reductions to their policyholders.

Many medical professionals experience difficulty finding the best insurance rate on their own. To find the best rate, you can speak with a professional who can help you select from the carriers in California.

Top Carriers in California

So what are some of the top carriers in California for you to consider? The following are some of the current top carriers in California:

1. The Doctors Company

One carrier you may want to work with is the Doctors Company. Considering how high defense costs can be, obtaining adequate protection is essential. In 1976, the Doctors Company was founded in response to the lack of availability and affordability in insurance for physicians. This insurance provider is physician-owned and serves more than 21,000 physicians across the U.S.

2. Medical Protective Company

Another carrier you may want to consider for your insurance needs is Medical Protective Insurance. This provider was formed in 1899, making it the oldest professional liability carrier in America. This carrier's AM Best rating is A++, also known as Superior. To keep yourself protected legally and financially, you may want to consider obtaining insurance from Medical Protective Insurance.

Additional top carriers include:

- Norcal Mutual Insurance Company

- The Cooperative of American Physicians - Mutual Protection Trust (CAP-MPT)

Though the top carriers can change over time, at Arthur J. Gallagher & Co., you can select from several carriers that we can help you connect with for the best coverage.

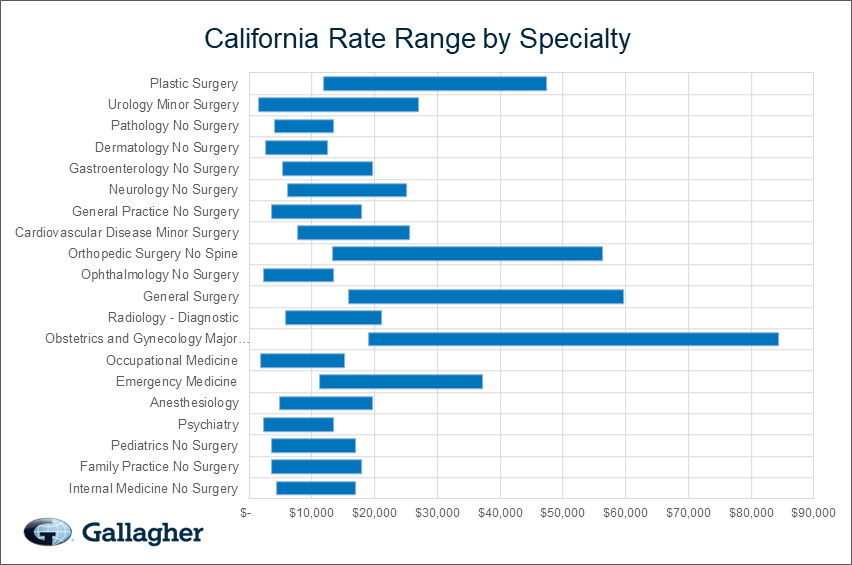

California Medical Malpractice Insurance Rates By Specialty (Top 20)

Rates depend greatly on specialty. Physicians offering high-risk care, such as surgeons, have higher rates than doctors in lower-risk areas. Prices will vary, though, based on your claim history and location in addition to your specialty. Always talk to an insurance expert to get a more specific quote for your malpractice insurance.

Below are undiscounted state filed rate data averages across all territories for 1,000,000/3,000,000 limits.

| Specialty | Average Rate | Lowest Rate | Greatest Rate | Count |

|---|---|---|---|---|

| Internal Medicine No Surgery | $8,772 | $4,407 | $16,876 | 13,085 |

| Family Practice No Surgery | $8,220 | $3,526 | $17,899 | 11,872 |

| Pediatrics No Surgery | $8,015 | $3,605 | $16,876 | 7,112 |

| Psychiatry | $5,181 | $2,203 | $13,501 | 5,800 |

| Anesthesiology | $11,806 | $4,848 | $19,689 | 5,437 |

| Emergency Medicine | $22,190 | $11,257 | $37,127 | 5,311 |

| Occupational Medicine | $6,700 | $1,763 | $15,215 | 5,231 |

| Obstetrics and Gynecology Major Surgery | $42,127 | $18,952 | $84,380 | 4,137 |

| Radiology - Diagnostic | $11,289 | $5,729 | $21,095 | 3,777 |

| General Surgery | $29,438 | $15,865 | $59,605 | 2,616 |

| Ophthalmology No Surgery | $6,400 | $2,203 | $13,501 | 2,543 |

| Orthopedic Surgery No Spine | $26,176 | $13,221 | $56,383 | 2,247 |

| Cardiovascular Disease Minor Surgery | $12,910 | $7,645 | $25,596 | 2,021 |

| General Practice No Surgery | $8,220 | $3,526 | $17,899 | 1,700 |

| Neurology No Surgery | $11,647 | $6,170 | $25,059 | 1,559 |

| Gastroenterology No Surgery | $10,268 | $5,288 | $19,689 | 1,542 |

| Dermatology No Surgery | $6,590 | $2,644 | $12,530 | 1,435 |

| Pathology No Surgery | $7,497 | $3,966 | $13,501 | 1,193 |

| Urology Minor Surgery | $14,462 | $1,516 | $27,001 | 1,170 |

| Plastic Surgery | $25,113 | $11,899 | $47,434 | 1,121 |

* Please note that the above rates are state filed rates. It is not uncommon for Gallagher Healthcare clients to receive up to 50% or more in discounts from state filed rates. Please Request a Quote to receive a custom premium indication.

Rate Range by Specialty

This chart compares the range of possible state filed medical malpractice premium rates by admitted markets and a few Gallagher Select markets broken out by the top 20 specialties in California.

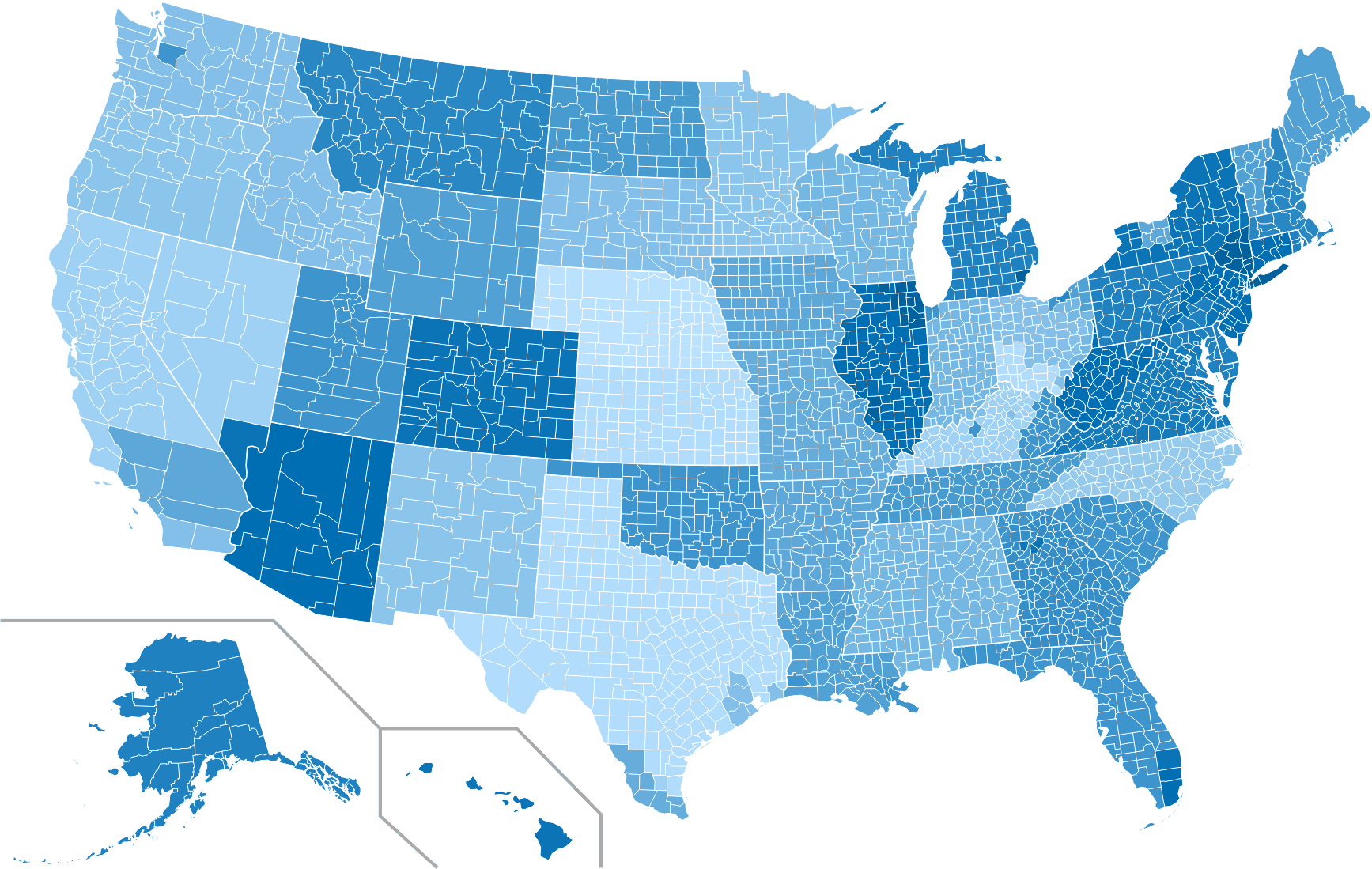

USA Ranking Map

The map below provides a visual display of the nation and compares what a typical primary care physician might pay compared to each individual state and county. This research is based on the average rate for a single specialty, the most common limits in that state, and the mature claims made premium. The darker the blue, the higher the average premium, see how California compares to other states.

Premium savings is just one click away! Complete this form to receive your FREE, NO OBLIGATION medical malpractice insurance quote. You can also call us at 800.634.9513 and ask to speak to a salesperson.